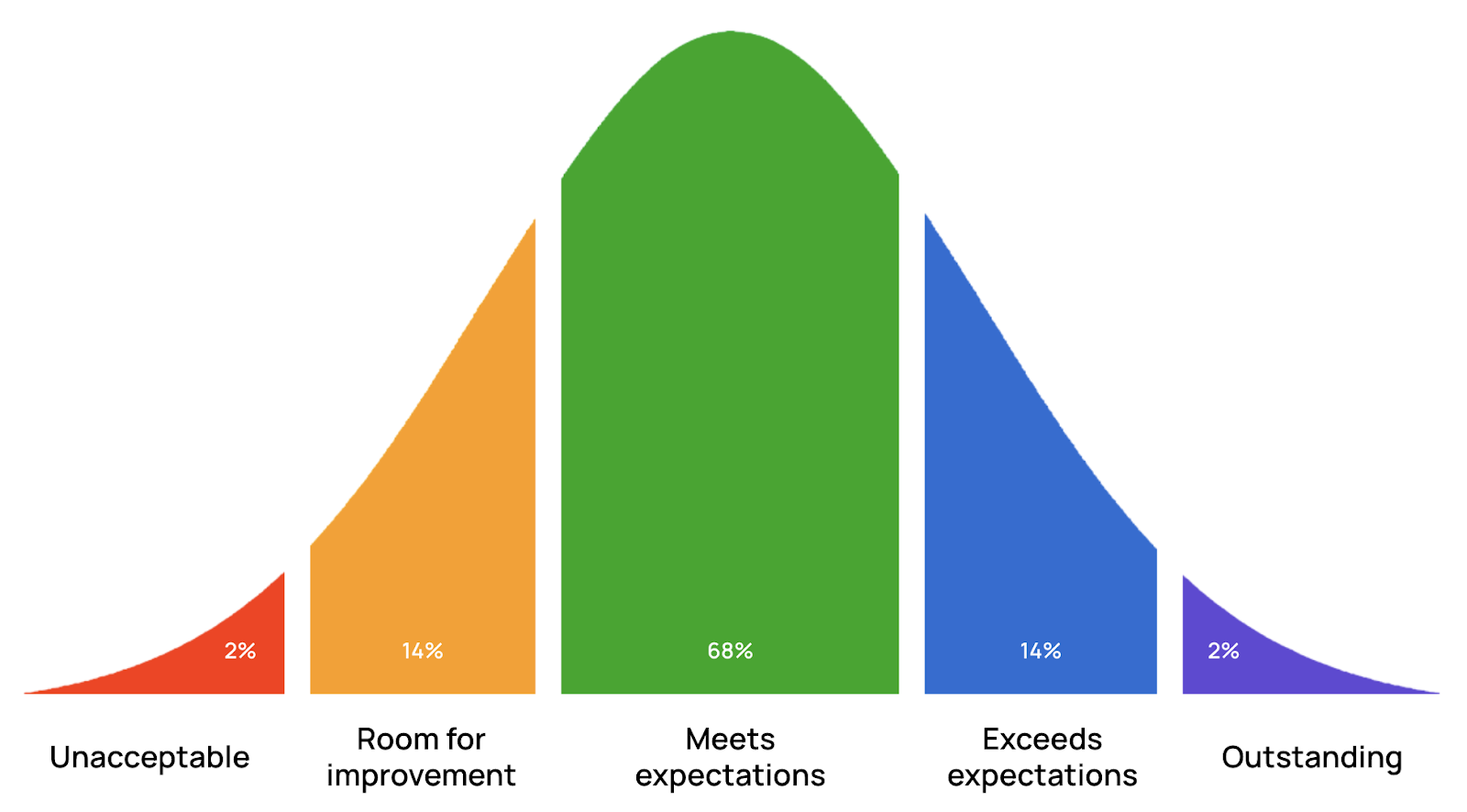

I ran across an important quote today that is particularly enlightening about attitudes towards investment returns. It relates to the Laplace-Gaussian distribution, but before I Explain further, ask yourself a question. If I tell you that a random variable did not follow a Laplace-Gaussian distribution, what is your emotional response to such a statement? It’s a pretty safe bet that the answer is “Nothing. Why would anybody respond to that? I don’t even know what it means.” But what if I told you that the random variable is a stock return, and that those returns are Abnormal. I am willing to bet that such a statement brings a very different idea to mind. The simple fact is that the Laplace-Gaussian Distribution and the Normal Distribution are simply two names for the same thing.

Laplace and Gauss were two famous mathematicians who did great theoretical work analyzing data and distributions and there was some disagreement over which should get the most credit for the understanding about what we now call the Normal distribution. Gauss may have even coined the term “Normal” in this context because he was referring to a technical idea known as “orthogonality”. If I consider a variable in 2-dimensional space, I would say that the X axis is “Orthogonal” to the Y axis and that movement along one axis can be thought of as having no impact on the measurement along the other. Some would say that these axes are “Orthogonal” to each other while others would say that they are “Normal.” In this context, these words mean the same thing. If this is all that the term “Normal” meant, it would be of little interest to us as investors.

At the beginning of the 20th century another author by the name of Karl Pearson wrote;

Many years ago I called the Laplace–Gaussian curve the normal curve, which name, while it avoids an international question of priority, has the disadvantage of leading people to believe that all other distributions of frequency are in one sense or another ‘abnormal’.

In other words, Pearson wanted to avoid the question of who should get the most credit (Laplace or Gauss) so he wanted to use a different name for the distribution. Unfortunately, he also recognized that he had opened a sort of “Pandora’s Box” because the words Normal and Abnormal, evoke an emotional response, that the label Laplace-Gaussian does not. This is a big deal because many of your investment decisions are not the result of some cold-detached analysis, but are actually emotional reactions. We buy because we are excited, and we sell because we are afraid. I have often felt that this was a particularly unfortunate turn of events for do-it-yourself investors, because we react to the word “Normal” in a funny way.

Consider this scenario. You are called in for at parent-teacher conference at which your 2nd grader is being discussed and the teacher says, “We just got the results back from a standardized test and your son’s score was at the median of the distribution, but is also a bit below the mean.” This is likely to lead to a discussion about tutoring, or additional study aids.

As an alternative, think about what happens if the teacher says, “We just got the results back from a standardized test and it is clear that your son is abnormal.” This is likely to lead to a discussion about how to get this teacher fired or how to get your son moved to a new school. The emotional response is orders of magnitude greater.

What’s this got to do with you and your money? When I say that the return on your diversified portfolio is likely to be Normally distributed that sounds reasonable and almost comforting. Note that I am not saying that the returns of the individual stocks within that portfolio are Normally distributed. Saying that the total comes from a normal distribution makes sense because the sum of a large number of random variables will have a normal distribution regardless of the distribution of the individual variables that went into the sum. In other words, having normally distributed portfolio returns says nothing about the distributions of the returns of the individual stocks that constitute that portfolio. The simple fact is that the total return of that portfolio is not driven by the typical stock – it is, in fact driven by the outliers.

This statement is true because the distribution of individual stock returns cannot be truly “Normal” because most returns are going to be below the average. This has to be true because the return distribution has a lower bound. The stock cannot lose more than 100% of its value. On the other hand, it can rise by thousands of percentage points. This explains why the typical stock will not show “Normal” performance. In fact, the typical stock “underperforms.” It is the tail events that drive everything.

When we look at income distributions, net worth distributions, and stock return distributions the Mean is going to be greater than the median. The median household income is about $74K, but the average is about $106K. The median household net worth is about $192K but the average is closer to $1 Million. This happens because the top 1% is so far above the rest of the population that it skews the distribution to the upside. The same thing happens with stocks. Imagine buying stocks in 100 different companies in January of 2000 and holding it until today. If one of those stocks happened to be Apple, the 29,000% return on that stock dramatically distorts the average making the average much higher than it was for the typical stock in the portfolio. Thus, the typical stock underperforms, just like the typical household (the household at the median) is about 20% below the average in terms of income and 90% below in terms of net worth.

Our mind has trouble dealing with this simple fact, even though it is overwhelmingly clear. Warren Buffet has frequently stated that he has invested in 400 – 500 companies over his career but almost all of his money has been made from the top 10 and nearly half of it came from his investment in Apple.

JP Morgan published a study of the Russell 3000 a few years ago and found that since 1980 about 40% of those stocks lost at least 70% of their value and never recovered. While roughly 100% of the portfolio return came from the top 7% of the stocks in the index. Results are not driven by the average firm – they are almost entirely driven by the outliers,

Of course, the obvious emotional response is, “I will just buy the outliers and win the game.” A great strategy that literally EVERY investor hopes to do and almost no investor will succeed at. This is true because, if it is obvious that firm Z is going to be a huge winner, the price of that stock will immediately reflect that fact, and your subsequent gains will be reduced because the starting price was so high. The winning stock (in terms of returns) is going to be the one that no one thinks is going to be the winner, that then turns out to be the outlier. This is why you can “buy low and sell high”. The stock price was low because no one thought it was going to do much. It became high as a pleasant surprise, and that’s where your real profit is. Buying Apple stock in 1997 when it sold for $3.50 a share (Yes, you read that correctly!) and holding it until today is the obvious way to win the game. “Well, why don’t I just buy that one?” Simple, because, you don’t know which one that will be. The outliers drive everything and your ability to find them before anyone else is like finding the needle in the haystack. That’s why we recommend that you simply buy the haystack and get the needle as part of the deal.

Oddly, we are comfortable with the idea that the outliers drive many things. We know that every NBA player is pretty literally 1 in a million, as is the best selling author, musician, or artist. But we have a hard time buying into that idea with stocks, perhaps because we feel that such an outcome would be “abnormal.”